The Investment Case for Private Credit

The primary attraction for private credit investors is the opportunity to earn a similar return to vanilla equities, with much lower volatility.

The Opportunity

Australian Small and Medium Enterprises (SMEs) are starved of capital primarily due to the continued reduction in banks’ lending appetite for lending coupled with a domestic debt capital market that lacks the scale and depth compared to overseas counterparts. This funding gap in the market provides private credit investors with opportunities to deploy capital into the sector through structures that protect capital while exhibiting excellent risk return profiles.

The 2021 SME Banking Insights Report, commissioned by Judo Bank and conducted by East and Partners showed that one in four SMEs is unsuccessful in obtaining finance. The third edition of the report which includes SMEs with a turnover of up to $50m found that the funding gap for this segment was $119.2 billion.

This is a result of changes to regulatory and prudential regimes which have seen banks reduce and withdraw offering credit particularly to the mid-market corporates and SMEs.

The gap also provides an opportunity for private credit managers to find high quality loans within the SME segment.

An emerging asset class

“Private credit managers, including many boutiques, have experienced staggering growth rates over the past three to four years as banks have restricted lending or failed to provide borrowers with the flexibility needed during the pandemic.”

Australian Financial Review, 2022

The Asset Class

Private credit refers to a range of debt investments that are available to companies or those requiring capital to fund specific projects. A borrower has obligations to make predetermined principal payments in addition to interest and fees which generate a return for the lender. The borrower has a contractual obligation to repay the capital at a pre-determined future date.

Private credit investments can deliver higher returns from a higher interest rate, upfront fees and in some cases attaching equity instruments over the underlying business that is borrowing the money. The investments are illiquid, in that they cannot be freely traded in a secondary market. This compares to other credit investment such as investment grade bonds and high yield bonds which can be traded in a secondary market but typically trade OTC, experiencing large bouts of volatility.

Investments are privately negotiated with the borrower and there are various features such as loan structures and controls to provide protection to the lender, as well as interest rates and the potential for complementary equity and options to generate additional returns.

The Investment Case

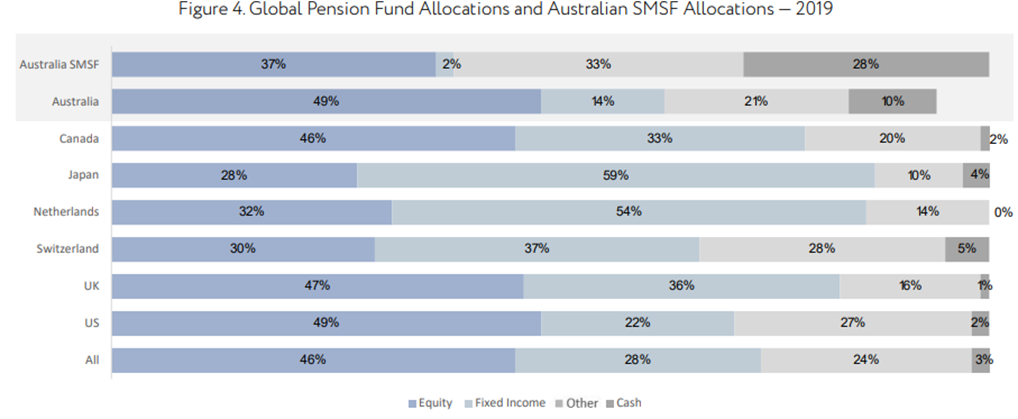

Private credit portfolios, if structured properly, have the potential to generate superior risk-adjusted returns relative to other asset classes. Australian investment portfolios are generally underweight fixed income at both institutional and individual investor levels compared to global investors. Australian portfolios have a 14% allocation to fixed income which decreases further when analysing Australian Self-Managed Super Funds’ 2% allocation to fixed income. This compares to 36% in the United Kingdom, 22% in the United States and 28% across the world.

There are numerous benefits associated with investing in private credit which include:

- Generating Sufficient Yield in a Low Interest Rate Environment

- Greater Protection from Rising Interest Rates

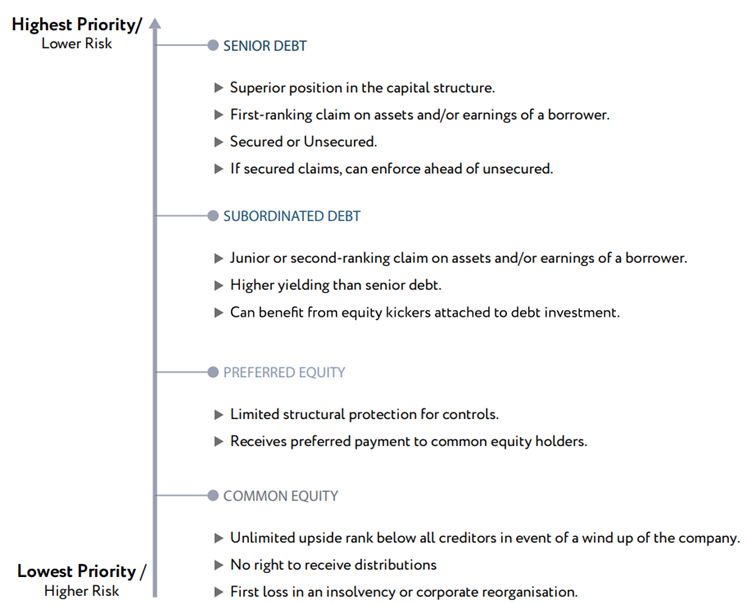

- Higher Seniority and Security

- Greater Lender Protections and More Control

- Lower Potential Losses in a Default

- Historically Low Allocation to Fixed Income in Australian Portfolios

- Asymmetric Return Profiles Through More Upside Potential

- Higher Illiquidity Premium

- Low Volatility

Private Credit in a Rising Interest Rate Environment

As interest rates rise, driven primarily by inflation, private credit provides several resilient characteristics that benefit investors. Firstly, pricing of private credit loans is a key feature, with variable loans benefiting from a rising interest rate environment. Interest rates based on a base rate plus a margin mean that investor income rises alongside interest rate increases. For loans priced with fixed interest rates, short duration loans is a mitigating factor, allowing the lender to reprice debt at higher interest rates as loans mature.

Another defensive characteristic is the underlying business model of the borrowers in the loan book. In high inflationary environments, a portfolio of companies that can pass on cost increases to customers and maintain margins, safeguarding investors against rising input costs such as wages and raw materials.

Loan origination is typically done via private negotiation, offering investors protection as lenders negotiate better terms, including a senior secured structure, covenants, and attaching equity exposure, each of which can make investments more defensive.

Private loans have also historically offered relatively low volatility as private credit managers are not forced to mark to market its assets daily due to constant re-pricing experience in tradable public markets. This provides more stable returns during periods of market volatility.

Finally, credit quality and fundamentals of issuers generally improve with economic recoveries, meaning private credit managers are generally well positioned for a rebound in economic activity once the new business cycle begins.

How to Access Private Credit Investments

There are a number of Australian private credit managers who have been investing in private credit via listed and unlisted managed funds. One way to gain access to this sector is via the Altor AltFi Income Fund (Fund), specialising in SME and mid-market corporate private credit.

The Fund invests in private credit instruments and has a target distribution rate of 10% p.a. payable quarterly. It has over 4 years track record and has achieved 11.54% p.a. (to 31 March 2022).

It has achieved this by undertaking a robust investment process, taking the time to have a deep understanding of every investment it makes including the borrower’s key drivers, asset position and funding requirements. The manager looks at credit opportunities through a private equity lens prior to moving to credit assessment.

The Fund works with management to design a loan structure that meets the objectives of both parties. These debt instruments could vary from senior secured facilities, equipment financing, acquisition financing, management buyouts or research and development lending.

Furthermore, Altor’s value-add and active management strategy seeks to mitigate risk and deliver on return maximisation by being actively engaged with the business post-transaction whether at the board level or in a strategic role.

Written by

Benjamin Harrison

Chief Investment Officer

Written by

Benjamin Harrison

Chief Investment Officer